This week, the total inventory of construction steel experienced a slight decline. The total rebar inventory decreased by 0.39% WoW, while the total wire rod inventory increased by 0.70% WoW. On the supply side, in the EAF steel mill sector, some steel mills have resumed production recently due to considerations of maintaining market share and safeguarding employee rights, while others have announced new maintenance plans due to expanding losses. According to the SMM survey, the operating rate of 50 electric furnace steel mills nationwide, which primarily produce construction materials, was 31.86%, up 0.48% from the previous period. The impact from maintenance of construction materials at blast furnace steel mills was 1.2642 million mt, a decrease of 4,700 mt WoW, indicating a slight increase in overall supply. On the demand side, mid-week, the Central Financial and Economic Commission held a meeting and issued an anti-cut-throat competition initiative. Meanwhile, there were rumors of production restrictions in Hebei and Yunnan provinces, causing rebar futures to surge significantly. The market trading atmosphere improved, releasing some speculative demand. Under these combined influences, the total inventory of construction materials continued to decline slightly this week.

This week, the total rebar inventory was 5.1467 million mt, a decrease of 19,900 mt WoW, or 0.39% (previous value: -0.36%). Compared to the same period last lunar year, it decreased by 2.1064 million mt, or 29.04% (previous value: -29.59%).

Table 1: Overview of Rebar Inventory

Data source: SMM

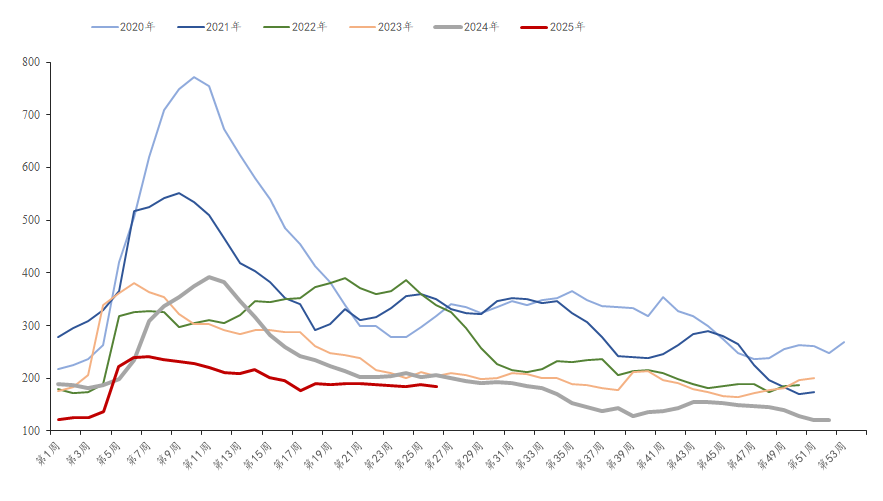

This week, the in-plant inventory of rebar was 1.8323 million mt, a decrease of 48,500 mt WoW, or 2.58% (previous value: +1.92%). Compared to the same period last year, it decreased by 109,900 mt, or 5.66% (previous value: -6.49%). On the supply side, the operating rate of EAF steel mills increased slightly, while the maintenance volume of blast furnace steel mills decreased slightly, resulting in an overall increase in supply. On the demand side, driven by the macro anti-cut-throat competition initiative and market rumors of production restrictions, steel traders' purchasing enthusiasm increased significantly. With more demand growth, the in-plant inventory of construction materials shifted from an increase to a decrease this week.

Chart-1: Overview of Rebar Factory Warehouse Inventory Trends from 2020 to 2025

Data source: SMM

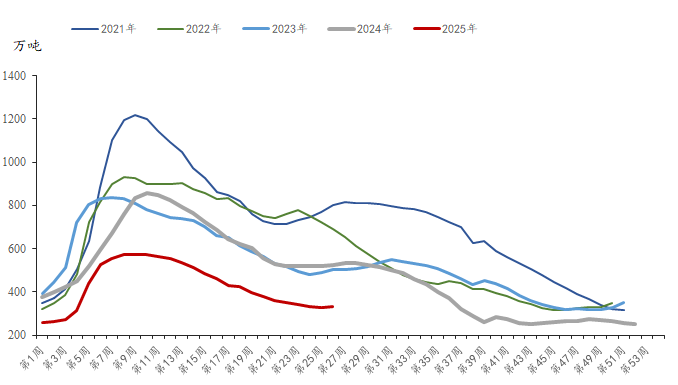

This week, the social inventory of rebar was 3.3144 million mt, an increase of 28,600 mt from last week, or 0.87% (previous value: -1.62%). Compared to the same period last year, it decreased by 1.9965 million mt, or 37.59% YoY (previous value: -38.31%). Boosted by macroeconomic and market news this week, traders' trading enthusiasm increased, and stockpiling was relatively active. However, due to the impact of high-temperature weather, the construction materials market is still in the off-season for demand. Terminal purchases are mainly based on rigid demand, and overall shipments are weak, resulting in a slight accumulation of social inventory.

Chart-2: Overview of Rebar Social Inventory Trends from 2021 to 2025

Data source: SMM

Looking ahead, on the supply side, EAF steel mills are still facing losses, and steel scrap prices remain high. It is expected that the operating rate will remain low. Blast furnace steel mills have moderate profits and high production enthusiasm. There is still an expectation for a decrease in the impact from maintenance, and supply is expected to increase slightly next week. Demand side, with the continuous high-temperature weather and blue rainstorm warnings issued in some regions, end-use demand is prone to decline rather than increase. Given the situation of increased supply and decreased demand, the fundamental contradictions in the building materials market will continue to accumulate, making it more difficult to reduce inventory. Therefore, it is expected that the total inventory of building materials will shift from a decrease to an increase next week.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)